Real wealth comes from systems you actively create — not shortcuts you hope will work.

The Passive Seduction

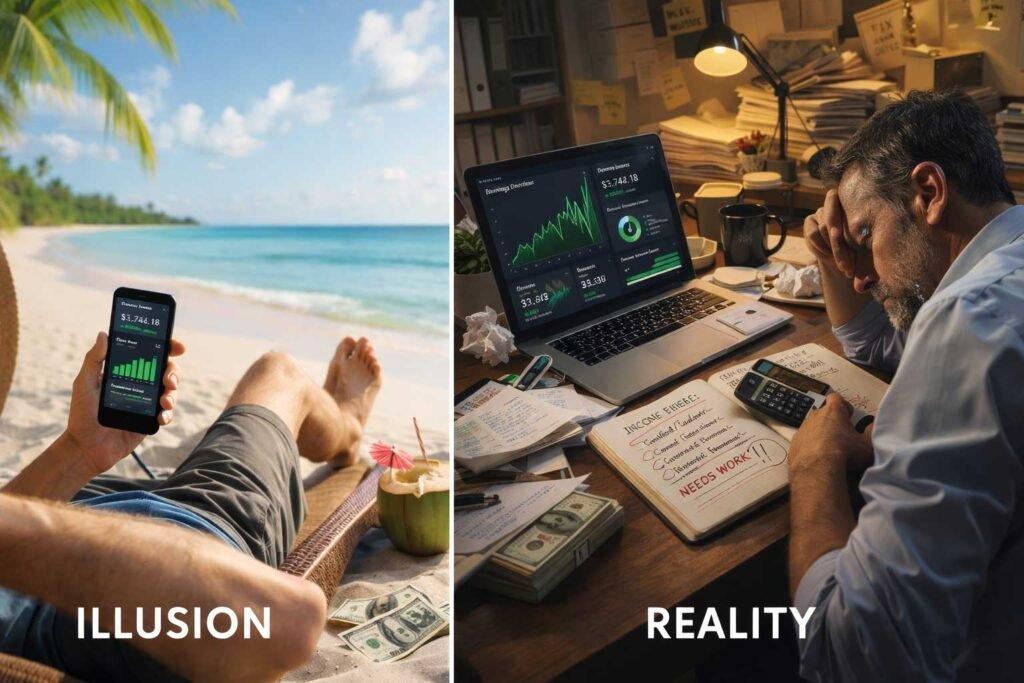

Every guru in a rented Lamborghini wants to sell you the same fantasy: make money while you sleep. Build passive income streams. Achieve financial freedom. Escape the 9-to-5 grind.

They’ll show you their bank statements (probably photoshopped). They’ll tell you about their rental properties generating ‘mailbox money.’ They’ll brag about YouTube ad revenue flowing in 24/7. They’ll flash dividend checks like winning lottery tickets.

Then they’ll offer to sell you their ‘proven system’ for $997. And thousands of desperate people buy it every single day.

Here’s what nobody tells you: that ‘passive’ rental income came with a 2 AM phone call about a burst pipe and an $8,000 repair bill. That YouTube revenue took seven years of making videos that got zero views. Those dividend stocks required $100,000 in capital most people don’t have.

BEHIND THE FACADE

But you know what they really make $50,000 a month from? Selling courses to people who believe passive income is actually passive.

The passive income industry is worth $250 billion and growing at 26% annually. By 2027, it’ll hit $500 billion. That’s not money from passive income itself—that’s money extracted from people chasing the dream.

As traditional job security vanishes, more people are realizing the necessity of the shift toward a multi-income world where passive streams aren’t just a luxury, but a survival strategy.

THE ‘SET IT AND FORGET IT’ LIE EVERYONE BELIEVES

Let’s talk about what ‘passive income’ actually means. The IRS defines it as earnings from rental properties, limited partnerships, or enterprises where you’re not actively involved. That’s the technical definition.

But marketers have weaponized that term to mean anything that isn’t a traditional 9-to-5 job. YouTube channel? Passive income! Rental property? Passive income! Online course? Passive income! Dividend stocks? Passive income!

This is where the scam lives. Because none of those things are actually passive.

According to analysis of U.S. households (Shopify, 2026), approximately 20% report some form of ‘passive income’ with a median earning of $4,200 per year. Not per month. Per YEAR.

The median household income in America is $83,730 (U.S. Census Bureau, 2024). So your ‘passive income’ represents about 5% of what you’d make showing up to a regular job.

Does that sound like the financial freedom they promised?

RENTAL PROPERTIES: THE ‘MAILBOX MONEY’ FANTASY

Real estate investors love talking about ‘mailbox money’—as if rent checks magically appear while they’re golfing in Tahiti.

Here’s what the actual data shows from studies of hundreds of thousands of landlords:

- Self-managing landlords spend 8-12 hours per month per property (Hemlane, 2018; iPropertyManagement, 2025)

- That breaks down to 3-5 hours dealing with tenant issues, 2-4 hours coordinating maintenance, 1-2 hours on rent collection, plus inspections, marketing, and paperwork

- 77% of landlords spend up to 20 hours monthly managing their properties

- 1.65% of landlords work full-time—160+ hours per month—on their ‘passive’ income

- The average landlord collected $34,217 in rental income but netted only $10,538 after expenses—a 30.8% profit margin (IRS data, 2018)

- Evictions cost an average of $3,500 each with a 14% eviction rate (iPropertyManagement, 2025)

- Tenant turnover costs $1,795 per unit every time someone moves out

- Annual maintenance costs range from $500 to $5,000+ per unit, with 12% of landlords spending over $5,000

So let me understand this: You’re working 8-20 hours a month, dealing with tenant drama and emergency repairs, and keeping only 31 cents of every dollar collected. And this is supposed to be passive?

You didn’t buy passive income. You bought a part-time job you can’t quit that occasionally floods your basement.

YOUTUBE: WHERE 90% OF CREATORS EARN NOTHING

Every YouTube success story you see is survivor bias dressed up as a business strategy. Let’s look at what the data actually shows:

- There are 69 million YouTube creators worldwide (VenueLabs, 2025)

- Only 3 million channels are monetized—that’s 4.3% (YouTube CEO Neal Mohan, 2024)

- To qualify for monetization, you need 1,000 subscribers AND either 4,000 watch hours in 12 months OR 10 million Shorts views in 90 days

- 90% of YouTube videos never reach 1,000 views (Highbrow Magazine analysis)

- Only 0.77%—less than one percent—of videos reach 100,000 views (DemandSage, 2025)

- Average creator earnings: $0.18 per view or $18 per 1,000 views (Descript, 2025)

- For 10,000 views monthly, you’re looking at $10-$300 depending on niche and audience location

- It takes an average of 7-8 YEARS of consistent effort to achieve significant recognition (DemandSage, 2025)

Let me translate this: You should spend 7-8 years making videos for free, competing against 69 million other creators, with a 95.7% chance you’ll never make a cent.

That’s not a business model. That’s a lottery ticket with worse odds.

The Three-Year Experiment Nobody Talks About

A documented case study (Vocals Media, 2024) tracked someone who spent three years systematically testing multiple passive income strategies with a $1,000 budget and 5 hours weekly commitment.

The results:

- Print-on-demand: 40 hours invested over 6 months → $0 earned

- Stock photography: 30 hours over 8 months → $3 total

- Affiliate website: 200+ hours, 50+ articles over 18 months → First 9 months: $0, Eventually: $80-120/month

- Digital eBook: 40 hours creating → $45-75/month with minimal maintenance

- Content royalties: Old blog posts → $15/month, truly passive

- Dividend investing: $1,000 invested → $22/month, 0.1 hours maintenance

Total monthly income after three years of work: $197.

That’s $2,364 annually. At that rate, replacing a $50,000 salary would take 21 years.

Sounds passive as hell, doesn’t it?

THE ONLY ACTUAL ‘PASSIVE’ OPTION: BE RICH FIRST

You want the closest thing to real passive income? Dividend stocks and REITs. But here’s the uncomfortable truth:

You need to already be rich.

A $100,000 investment in a REIT yielding 6% generates $6,000 per year. That’s $500 monthly. Not bad, right?

Except you needed ONE HUNDRED THOUSAND DOLLARS to start.

Most people searching for ‘passive income’ are doing so because they DON’T have $100,000 lying around. That’s the entire point. They’re looking for a way to build wealth without massive capital.

It’s like telling a hungry person that caviar tastes amazing. Cool insight. Where’s my hundred grand?

And even dividend investing isn’t truly passive:

- You need to analyze dividend yields, payout ratios, and cash flow coverage

- Review quarterly earnings reports and industry trends

- Rebalance your portfolio periodically

- Stay updated on tax law changes affecting dividend income

Oh, and dividends aren’t guaranteed. In 2020, 68 out of 380 dividend-paying S&P 500 companies cut or suspended their dividends (Charles Schwab data). Macy’s stock dropped 80% over 10 years and suspended dividends entirely in March 2020.

So the most ‘passive’ option still requires capital most people don’t have and ongoing work most people don’t want to do.

HOW THE SCAM BECAME A QUARTER-TRILLION-DOLLAR INDUSTRY

This didn’t happen overnight. The passive income industrial complex was built systematically over decades:

Phase 1: The Foundation (1990s-2000s)

Robert Kiyosaki writes ‘Rich Dad Poor Dad,’ sells 32 million copies, and popularizes the concept of ‘making money work for you.’ The idea is legitimate—but it plants the seed that anyone can do it easily.

Phase 2: The Platform Gold Rush (2005-2015)

YouTube launches in 2005. Blogging platforms and e-commerce explode. The early adopters—people who got in when nobody knew what these platforms would become—actually do build passive income.

But they did it through years of unpaid labor when these platforms were unproven and competition was minimal. Their success stories become the blueprint everyone tries to replicate.

The problem? The window has closed. The platforms are saturated. The easy money is gone.

Phase 3: The Meta-Economy (2015-2020)

Successful creators realize they can make MORE money teaching people how to build passive income than from their actual passive income streams.

The affiliate marketing industry hits $18.5 billion by 2024 (Hostinger, 2025). The product becomes the dream itself. They’re not selling rental properties—they’re selling courses about rental properties.

Phase 4: Desperation Meets Marketing (2020-Present)

COVID hits. Inflation spikes to 9.1%—the highest since 1981 (U.S. Bureau of Labor Statistics). Rent outpaces wages by 270% (The Zebra, 2026). People need to work 155 hours weekly at minimum wage just to afford a basic apartment.

The side hustle economy explodes to $556.7 billion, with 36% of Americans scrambling for extra income (Hostinger, 2025).

Desperate people make excellent customers for passive income courses.

The industry reaches $250 billion, growing at 26% annually. By 2027, it’ll be half a trillion dollars (Uscreen, 2025).

And almost none of that money comes from passive income itself. It comes from selling the dream to the next wave of believers.

THE FIVE LIES KEEPING YOU BROKE

Lie #1: ‘It’s Easy Money with Minimal Effort’

Show me one person who built meaningful passive income with minimal effort. I’ll wait.

Every legitimate passive income stream requires massive upfront work, ongoing maintenance, or both. Academic research shows it takes hundreds to thousands of hours before seeing meaningful returns (Johnson et al., 2019; Moore & Thompson, 2020).

The term ‘passive’ describes what the income does once established—not what you do to establish it.

Lie #2: ‘You Can Quit Your Job’

That $4,200 median passive income? Even successful side hustlers averaging $891 monthly (Hostinger, 2024) are making $10,692 annually.

The median household income is $83,730 (U.S. Census Bureau, 2024).

You’re going to quit your job for 13% of what you currently make? That’s not financial freedom. That’s financial suicide.

Lie #3: ‘Everyone Can Do It’

Success requires capital, skills, sustained effort, and risk tolerance. Research shows that gender, age, education, marital status, and income all significantly influence investment outcomes (Arora & Marwaha, 2014; Jariwala, 2015).

Not everyone starts from the same place. Pretending otherwise is gaslighting wrapped in motivational quotes.

Lie #4: ‘It’s Passive Once Built’

Nothing stays passive. Properties need maintenance. Algorithms change. Markets shift. Technology evolves. What worked yesterday becomes obsolete tomorrow.

Call it what it actually is: leveraged income. One unit of effort producing multiple units of income. But it’s never truly hands-off.

Lie #5: ‘Passive Income Equals Financial Freedom’

Passive income is volatile. Markets crash. Tenants vanish. Algorithms destroy channels overnight.

Unlike traditional employment, you get no health insurance, no retirement benefits, no legal protections, and no stability.

Using it as your sole income source without massive reserves is financial Russian roulette.

WHAT ACTUALLY WORKS: THE UNCOMFORTABLE TRUTH

Passive income isn’t a scam. It’s a marketing term for something that requires massive active work.

Here’s when it genuinely works:

When you already have substantial capital: That $100,000 REIT investment? Great if you have it. Since 1960, reinvested dividends and compounding have accounted for 85% of the S&P 500’s cumulative total return (Hartford Funds, 2025). A $10,000 investment in 1993 with reinvested dividends would have grown to $182,000 by 2023—versus $102,000 without reinvestment (Charles Schwab). But you need capital to capitalize on capital.

When you’re willing to front-load 1-2 years of intense work: Digital products, authority websites, rental properties can generate reduced-effort income—but only after putting in 10-20 hours weekly for years. This isn’t passive. It’s deferred compensation.

When you leverage existing expertise: Photographer selling stock photos. Developer creating plugins. Investor building a dividend portfolio. If you’re already skilled, you skip the learning curve. But you still do the work.

When your goal is supplementary income: An extra $200-500 monthly? Totally achievable and genuinely helpful. This is where ‘passive income’ shines—as a supplement, not a replacement. But don’t quit your day job.

THE REAL FRAMEWORK: BUILD SYSTEMS, NOT DREAMS

If you’re serious about building alternative income—not chasing fairy tales—here’s the actual roadmap:

Step 1: Get Brutally Honest About Your Reality

How much time do you actually have? Not what you wish you had. What you actually have after work, family, sleep, and basic human needs.

How much capital can you invest without screwing yourself? Not what you could scrape together by emptying your emergency fund. What you can afford to lose completely.

What skills do you already have? Don’t start from zero if you don’t have to.

Can you handle income volatility? Be honest. Some people can’t sleep when their income fluctuates. If that’s you, passive income will wreck your mental health.

Step 2: Match Strategy to Resources

Got capital, no time? Index funds, dividend stocks, REITs. Boring but effective.

Got time, no capital? Content creation or skill-based products. Expect 2-5 years before seeing returns. Not months. YEARS.

Got both time and capital? Real estate could work. But factor in 8-10% for property management costs or accept you’re working 8-20 hours monthly.

Got neither? Stop chasing passive income and focus on increasing your primary income. Get better at your job. Negotiate raises. Switch companies. Learn higher-value skills. Build a foundation first.

Step 3: Process Goals Over Outcome Goals

Don’t set a goal of ‘$2,000/month passive income.’ That’s fantasy thinking. Set process goals you can control:

- ‘Publish 2 blog posts weekly for 12 months’

- ‘Invest $500 monthly in dividend stocks’

- ‘Study real estate investing 5 hours weekly’

Process goals keep you moving when results don’t show up for months or years.

Step 4: Track Everything Like Your Life Depends On It

Time invested. Money spent. Results achieved—even if zero. Lessons learned.

This data lets you make rational decisions instead of falling victim to the sunk cost fallacy. If something isn’t working after six months of consistent effort, you have data to prove it. Cut your losses and move on.

Step 5: Call It What It Actually Is

Stop calling it ‘passive income.’ The word is poisoned. Use accurate terms:

- Front-loaded effort: Work your ass off now for potential future returns

- Leveraged income: One effort produces multiple income units

- Alternative income: Diversification, not replacement

- Long-term project: Multi-year commitment, not a weekend side hustle

Reframing prevents the disappointment that comes from unrealistic expectations.

Step 6: Build Safety Nets or Get Wrecked

Before you chase alternative income:

- 6-12 month emergency fund (non-negotiable)

- Keep your day job until alternative income is stable for at least 12 months

- Only invest what you can afford to completely lose

- Have backup plans for when (not if) things fail

- Maintain insurance coverage (health, liability, property)

Safety nets separate calculated risk from stupidity.

THE BOTTOM LINE: BUILD IT, DON’T BUY IT

Passive income exists. But it’s not what they’re selling you.

The people with genuine alternative income streams didn’t buy a $997 course and follow a blueprint. They spent years building systems through trial and error, massive upfront work, substantial capital investment, or all three.

They built it. They didn’t buy it.

And here’s the part nobody wants to hear: traditional employment isn’t a failure state. It’s not something you need to escape from. Trading time for money isn’t a character flaw—it’s how civilization has worked for thousands of years.

If building alternative income doesn’t fit your current situation, resources, or risk tolerance? Focus on optimizing what you already have. Get better at your job. Negotiate harder. Learn more valuable skills. Build a stronger financial foundation.

The goal isn’t ‘passive income’—it’s financial security and life satisfaction. How you get there is your choice.

Just make that choice based on verified data, not marketing designed to separate you from your money.

If you made it this far, CONGRATULATIONS! Thanks for sticking around and taking time out of your day. I truly appreciate you. If you want to take control of your life and you want updates when more of my articles come out, Subscribe below and if you want to actually participate in these conversations head to my channel.

Cheers!

Adam

DISCLAIMER: This article is for educational and informational purposes only. It does not constitute financial, investment, tax, or legal advice. Always consult a qualified financial advisor before making investment decisions. Past performance is not indicative of future results.